Why Malaysia's Fintech Isn't Ethical by Default

Malaysia’s fintech boom looks promising but is it ethical by design? This post explores hidden assumptions, transparency failures, and why local isn’t always trustworthy.

Everyone says Malaysia's fintech is booming.

New digital banks. Innovative payment solutions. Financial inclusion initiatives. Investment flowing in.

The growth numbers look impressive. The innovation stories sound exciting.

But nobody asks the harder question: is it ethical by design?

Most Malaysian fintech assumes that being compliant means being ethical. That serving local users means serving them well.

That innovation automatically improves lives.

These assumptions are wrong. And they're costly.

The Hidden Assumption

There's a belief that local fintech is inherently more trustworthy than global alternatives.

Malaysian companies understand Malaysian needs. They're regulated by local authorities. They serve local communities.

This sounds reasonable. But geography doesn't guarantee ethics.

A local app that uses dark patterns to encourage overspending is still exploitative.

A Malaysian lending platform with opaque risk scoring still harms users who get rejected without explanation.

Being local doesn't make you ethical by default.

Where Ethics Actually Break Down

Malaysian fintech has real blind spots that compliance doesn't catch:

Transparency Gaps

Most financial apps don't explain how they make decisions.

Why was your loan rejected? How is your credit score calculated? What data influenced the algorithm's choice?

Users get outcomes without understanding. This creates frustration, suspicion, and a sense of powerlessness.

Transparency isn't just about legal disclosure. It's about giving people the information they need to make informed decisions about their own money.

Shariah Compliance vs. Ethical Design

Many Malaysian fintech products advertise Shariah compliance as an ethical selling point.

But Shariah compliance is about religious law, not comprehensive ethics.

You can have a Shariah-compliant product that still uses manipulative design, charges hidden fees, or targets vulnerable users.

Religious compliance and ethical design are related but different concerns. Both matter. Neither guarantees the other.

Inclusion Without Protection

Financial inclusion is a worthy goal. Getting underserved populations access to financial services matters.

But inclusion without safeguards can cause harm.

Offering microloans to people who can't afford them isn't inclusion; it's exploitation.

Making credit cards available without proper financial literacy support creates debt traps, not opportunities.

Real inclusion means designing products that help people improve their financial lives, not just access more financial products.

Why Compliance Isn't Enough

Malaysian fintech companies focus heavily on regulatory compliance.

Bank Negara requirements. Securities Commission guidelines. Anti-money laundering protocols.

This is necessary. Regulation exists for good reasons.

But compliance is about avoiding legal penalties. Ethics is about preventing harm before regulation arrives.

Most compliance frameworks are reactive. They respond to problems that have already happened. Ethical design is proactive. It tries to prevent problems from happening.

You can be fully compliant and still build products that harm users in ways the law doesn't yet recognise.

The Cost of Ignoring Ethics

When fintech products cause harm, the consequences go beyond individual users:

Trust erosion spreads quickly in Malaysia's connected society. One bad experience gets shared widely. Trust, once lost, is expensive to rebuild.

Regulatory backlash happens when enough people complain. New restrictions. Stricter oversight. Higher compliance costs for everyone.

Talent flight occurs when good people don't want to work for companies with questionable ethics. The best builders choose employers they can be proud of.

Investment hesitation grows as ESG considerations become more important to funding decisions.

The market rewards ethical behaviour over time. But it punishes unethical behaviour quickly.

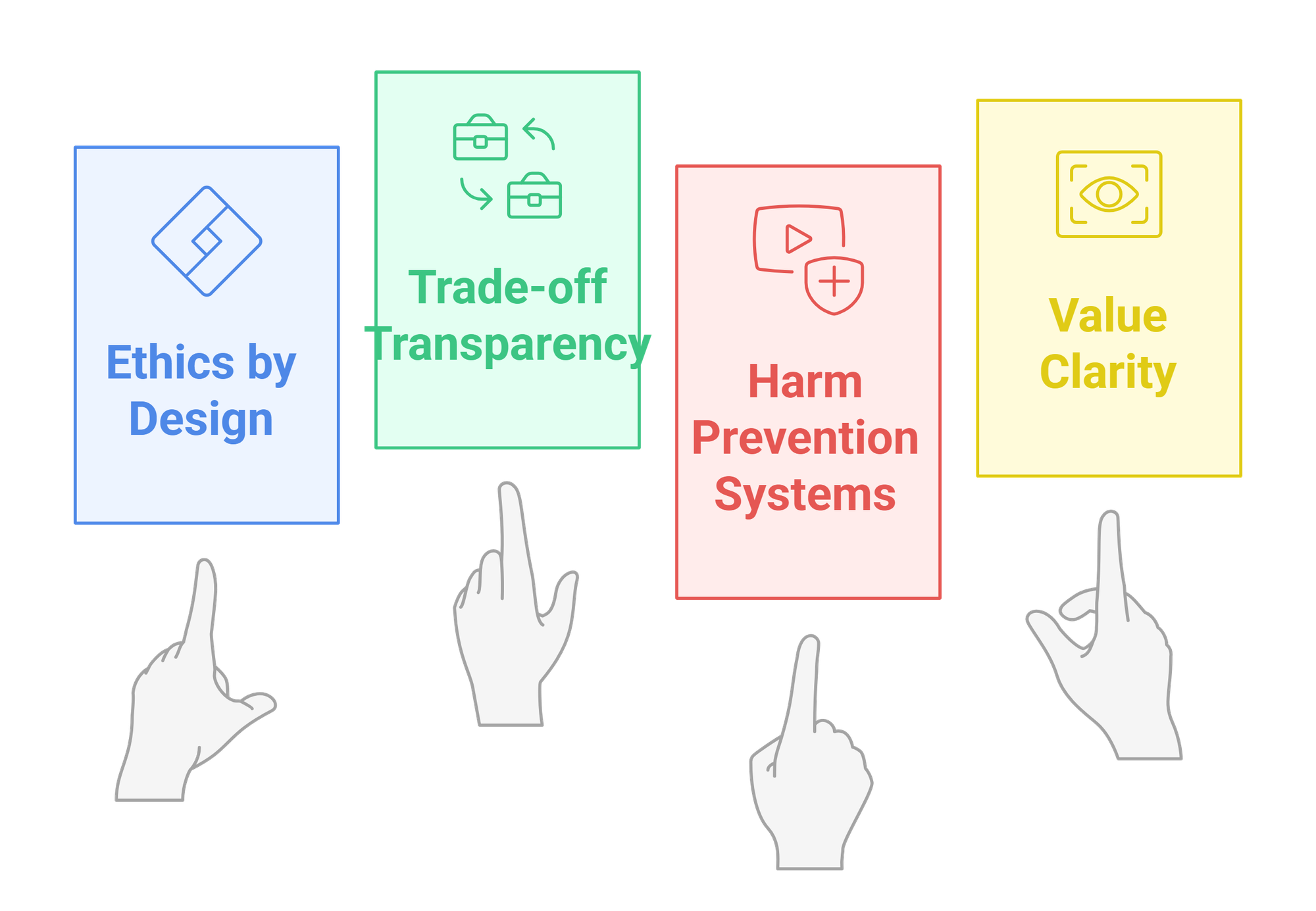

What Ethical Fintech Actually Requires

Real ethical fintech isn't about good intentions. It's about good constraints.

Ethics by design, not by addition. Ethical considerations have to shape the product from the beginning. You can't bolt ethics onto an exploitative business model.

Trade-off transparency. Every financial product makes trade-offs. Lower fees might mean less customer service. Faster approval might mean higher risk.

Users deserve to understand these trade-offs.

Harm prevention systems. What happens when users can't pay back loans? How do you prevent people from borrowing more than they can afford? How do you detect and prevent fraud?

Value clarity. What is the product actually optimising for? Profit? User welfare? Market share?

Users should know where their interests align with the company's interests.

These aren't nice-to-have features. They're core requirements for sustainable fintech.

The Malaysian Opportunity

Malaysia is in a unique position to lead in ethical fintech.

Our cultural values emphasise community, responsibility, and long-term thinking. These align well with ethical business practices.

Our regulatory environment is sophisticated enough to enforce standards but flexible enough to encourage innovation.

Our market is diverse enough to test products across different user segments and cultural contexts.

We could build fintech that's more ethical than global alternatives, not just more local.

But this requires choosing ethics as a competitive advantage, not treating it as a compliance burden.

Why This Matters Now

Malaysian fintech is scaling rapidly. Moving from early adopters to the mass market. From simple payments to complex financial products.

The ethical gaps that were manageable at a small scale become dangerous at a large scale.

A loan algorithm that makes unfair decisions for 1,000 people is a problem. The same algorithm making unfair decisions for 100,000 people is a crisis.

Once public trust is broken, it's hard to rebuild. It's better to design for trust from the beginning.

Where I Stand

I work in fintech, ethics, and AI systems.

I see the daily tension between moving fast and building responsibly. Between serving users and serving shareholders. Between innovation and protection.

These tensions are real. They can't be resolved with good intentions alone.

They require design discipline. The commitment to build ethical constraints into systems, not around them.

Malaysia has the talent to build ethical fintech. The question is whether we choose to prioritise it.

This blog is where I explore that choice. Publicly. Carefully. One tension at a time.

Because the stakes are too high to leave ethics to chance.

The future of Malaysian fintech depends on whether we can build trust as efficiently as we build features.

That's the challenge. And the opportunity.

This space stays independent. If it sparked value, you can fuel the next one ⇢

☕ Buy me a coffee